Understanding the implications of the current low interest rate environment on retirement funding is a must to ensure you can fund your desired retirement lifestyle.

Retirees usually implement more conservative investment strategies. The current ultra-low interest rates mean these more conservative approaches yield lower returns. This in turn increases the amount of capital required to fund a given retirement lifestyle.

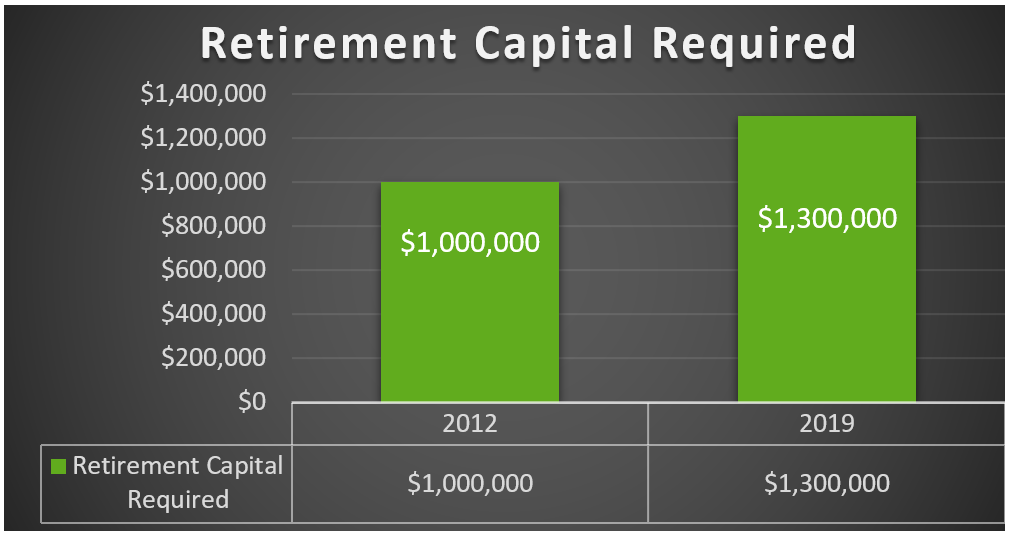

Consider that in 2012, retirees (aged 65) with $1 million could invest in a lifetime income stream that would guarantee them an income of $54,800 per year for the rest of their lives.

Today to implement the same investment strategy the client would need an additional $300,000 to obtain the same annual income level of $54,800. This increase of 30% in the capital required by retirees is significant – and may result in people in this position having to either defer their retirement to save the additional capital or implement strategies to save the additional funds in their pre-retirement years.

The above illustration does not factor the ever increasing costs of living (inflation).

In 2012, ASFA’s recommended budget for a ‘comfortable lifestyle’ for a retired couple was approximately $55,080 (approximately the same as the income stream implemented in the example above).

ASFA now suggests that retired couples will now need $61,522 per year to maintain that same ‘comfortable lifestyle’. The capital required to fund this level of income using the same income stream strategy would require an investment of over $1,500,000.

There are different strategies available to maximise your investment return, please contact our Financial Planning team on 8419 9800 for more information.